Divorce is a significant life event that reshapes the financial landscape for both parties. For solicitors advising clients through separation and settlement, cashflow planning offers a powerful, data-driven approach to support informed decision-making and long-term financial stability.

Used effectively, cashflow modelling can provide clarity, reduce conflict, and help assess the sustainability of proposed settlements. It is increasingly recognised by financial planners and legal professionals as a valuable tool in both pre- and post-divorce financial planning.

What is cashflow planning?

Cashflow planning involves projecting an individual’s financial position over time, incorporating income, expenditure, assets, liabilities, and key life events. The resulting model provides a visual representation of how financial decisions made today may impact future outcomes.

In the context of divorce, cashflow planning can be used in two distinct ways:

- Personal planning – to help an individual understand their financial future post-divorce.

- Impartial analysis – to support fair division of assets and assess the viability of proposed settlements.

How does it work?

1. Visualising financial futures

Cashflow modelling helps clients understand the long-term implications of settlement decisions. It can illustrate how choices such as retaining the family home or receiving a pension share will affect financial security over time.

2. Assessing settlement sustainability

Cashflow planning can be used to evaluate whether proposed arrangements are financially viable. For example, can one party afford to retain the family home? Will a pension sharing order provide sufficient retirement income?

3. Determining support needs

Cashflow models can assess the affordability and sustainability of spousal or child maintenance payments. This ensures that support obligations are realistic and fair to both parties.

4. Reducing conflict

By providing objective, evidence-based insights, cashflow planning can reduce emotionally driven decision-making. It supports more amicable negotiations and can be a useful tool in mediation or collaborative law settings.

5. Post-divorce financial planning

Following the final order, cashflow planning continues to play a vital role. It can be used as part of the advice process to help prepare for the future, along with immediate and longer-term advice needs. For example, the sale of the family home, or implementation of pension sharing orders, preparing for retirement or other financial goals.

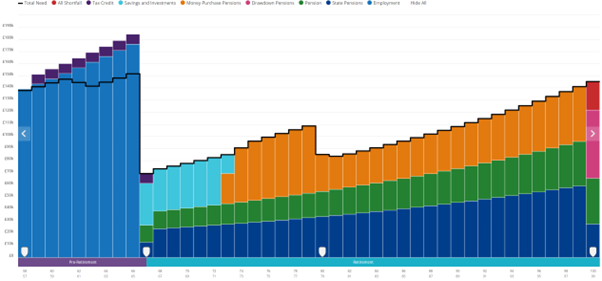

What does it look like?

It’s important to note that the tool is based on assumptions and is adjusted throughout the years to accommodate changes in legislation, cost of living and changes in the client’s circumstances.

Client outcomes: clarity, confidence, control

Cashflow planning empowers clients with three key outcomes:

- Clarity – a clear view of how their financial future may unfold year by year.

- Confidence – understanding the impact of key decisions on long-term financial wellbeing.

- Control – the ability to test different scenarios, such as downsizing, delaying retirement, or adjusting spending.

For solicitors, integrating cashflow planning into the divorce advice process can enhance the quality of financial guidance provided to clients. It supports fair settlements, reduces uncertainty, and helps clients transition into the next chapter of their lives with greater financial confidence.

Collaboration with financial planners who specialise in cashflow modelling can be particularly beneficial, ensuring that legal advice is complemented by robust financial analysis.

Chloe Platts is a Chartered Financial Planner at Benchmark Financial Planning

This article does not constitute tax, legal or financial advice and should not be relied upon as such. Tax treatment depends on the individual circumstances of each client and may be subject to change in the future. For guidance, seek professional advice.